The Veterans Deserve Homes Project

Help Support Our Mission to Prevent Veteran Homelessness

Veterans Deserve Homes Project – Providing Assistance to Low-Income Disabled Veterans Who Need Financial Help to Close their VA Home Loans!

Please Consider Donating to Our Veterans Deserve Homes Project to Make Sure Every Low-Income Disabled Veteran Has Access to Stable Housing Through Homeownership.

About Us

Many low-income disabled veterans qualify to use their VA Home Loan Benefits, however, they may be unable to finalize a home purchase without some financial assistance to pay for the expenses associated with a VA Home Loan. These expenses include Appraisal Fees, Termite Inspections, Home Inspections, Title Fees, and others. These fees are typically very low for a VA Home Loan but for some lower-income disabled Veterans, they are cost-prohibitive. Creative Drill Sergeants is raising funds through our fiscal sponsor Technical Assistance Partnership of Arizona to assist low-income disabled Veterans to pay some or all of these fees to ensure we get them the housing stability they need and deserve.

Donate Now

If you are a low-income disabled Veteran and would like to apply for assistance with VA Home Loan fees please email vdh@creativedrillsergeants.org or call us at 602-842-4400 option 1

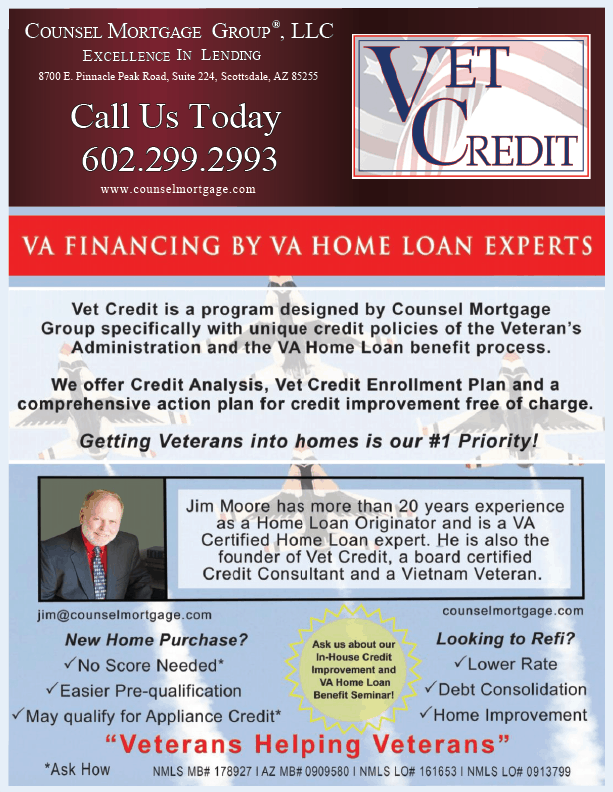

Vet Credit – A Free VA Home Loan Credit Counseling Service to Get Veterans and their Families On the Path to Homeownership

Sponsored by Counsel Mortgage Group

AZ LO #0913799 NMLS #161653

AZ MB #0909580 NMLS #178927

Are you a VA Home Loan eligible Veteran or Spouse in need of credit improvements to qualify for a new loan or refinance an existing VA Home Loan?

Have you been denied by a lender in the past?

Let Vet Credit help you qualify to use your VA Home Loan Benefits.

Our mission is to help place you on a pathway towards VA Home Loan qualification with lower interest rates through proper credit counseling.

We offer, Free of Charge, Vet Credit Enrollment for a Credit Analysis and a Comprehensive Action Plan for Credit Improvement!

Contact the Vet Credit Team

(602) 348-9475

Or, Send Us a Message to Get Started!

The VA Home Loan; the best loan in the mortgage loan industry.

Here’s why you should be using yours!

*No Minimum Credit Score

*No Mortgage Insurance

*Competitive Interest Rates

*Housing Allowance for Active Duty Military

*No Prepayment Penalty

*Ask Me About Alternative Credit*No Minimum Credit Score

*No Mortgage Insurance

*Competitive Interest Rates

*Housing Allowance for Active Duty Military

*No Prepayment Penalty

*Ask Me About Alternative Credit

Vet Credit uses credit improvement techniques, responsible budgeting, and sound credit decisions to help veterans obtain their VA Home Loan Benefits.

Veterans with satisfactory credit, sufficient income, and a valid Certificate of Eligibility (COE) may meet the requirements for a VA Home Loan, Cash-out refinance or an Interest Rate Reduction Refinance Loan.

Let us help you access resources to become a homeowner or refinance your existing home loan.

Jim Moore is a Vietnam Veteran paying it forward with this VET Credit Free Program as his way of recognizing his fellow veterans and giving the required professional attention they deserve. It is Jim’s personal touch that makes the VA Home Loan experience the most gratifying.

Jim Moore is a licensed Mortgage Loan Originator through the Arizona Department of Financial Institutions. Jim has 18 years of mortgage loan experience in all types of residential loans but is especially passionate about VA home loans.Jim has a proven track record of helping other veterans apply for and obtain VA Home Loan benefits. Whether it is purchasing or refinancing, Jim is an expert credit analyzer who will give you a written credit analysis, a written action plan, a personal credit consultation, and a pre-qualification letter once approved.

COUNSEL MORTGAGE GROUP,® LLCEXCELLENCE IN LENDINGJIM MOORE – LOAN ORIGINATOR(602) 299-3299www.counselmortgage.comJim@counselmortgage.com88700 E. Pinnacle Peak Rd. #2244 Scottsdale, AZ 85255AZ LO #0913799 NMLS #161653AZ MB #0909580 NMLS #178927

VA Home Loan Eligibility

You must have satisfactory credit, sufficient income, and a valid Certificate of Eligibility (COE) to be eligible for a VA-guaranteed home loan. The home must be for your own personal occupancy. The eligibility requirements to obtain a COE are listed below for Service members and Veterans, spouses, and other eligible beneficiaries.

VA home loans can be used to:

- Buy a home, a condominium unit in a VA-approved project

- Build a home

- Simultaneously purchase and improve a home

- Improve a home by installing energy-related features or making energy efficient improvements

- Buy a manufactured home and/or lot

- To refinance an existing VA-guaranteed or direct loan for the purpose of a lower interest rate

- To refinance an existing mortgage loan or other indebtedness secured by a lien of record on a residence owned and occupied by the veteran as a home

Eligibility Requirements for VA Home Loans

Service during wartime:

| World War II – September 16, 1940 – July 25, 1947 |

| Korean War – June 27, 1950 – January 31, 1955 |

| Vietnam War – August 5, 1964 – May 7, 1975 |

Service Requirements:

|

| Gulf War – August 2, 1990 – to be determined |

Service Requirements:

|

Service during peacetime:

| All – July 26, 1947 – June 26, 1950 and February 1, 1955 – August 4, 1964 |

| Enlisted – May 8, 1975 – September 7, 1980 |

| Officers – May 8, 1975 – October 16, 1981 |

Service Requirements:

|

If you were separated from service:

| Enlisted – After September 7, 1980 |

| Officers – After October 16, 1981 |

Service Requirements:

|

* 90 days applies for wartime

Active-duty service personnel:

| If you are now on active duty, eligibility can be established after 90 days of continuous active duty. Upon discharge or release from active duty, eligibility must be reestablished. |

Selected Reserve or National Guard:

If you are not otherwise eligible and you have completed a total of six credible years* in the Selected Reserve or National Guard (member of an active unit, attended required weekend drills and two-week active duty for training) and one of the following:

*Individuals who completed less than six years may be eligible if discharged for a service-connected disability. |

You may also be determined eligible if:

Note: A surviving spouse who remarries on or after age 57 and on or after December 16, 2003, may be eligible for the home loan benefit. However, a surviving spouse who remarried before December 16, 2003, and on or after age 57, must have applied no later than December 15, 2004, to establish eligibility. |

Spouses

The spouse of a Veteran can also apply for home loan eligibility under one of the following conditions:

- Unremarried spouse of a Veteran who died while in service or from a service connected disability, or

- Spouse of a Servicemember missing in action or a prisoner of war

- Surviving spouse who remarries on or after attaining age 57, and on or after December 16, 2003

(Note: a surviving spouse who remarried before December 16, 2003, and on or after attaining age 57, must have applied no later than December 15, 2004, to establish home loan eligibility. VA must deny applications from surviving spouses who remarried before December 6, 2003 that are received after December 15, 2004.) - Surviving Spouses of certain totally disabled veterans whose disability may not have been the cause of death

Other Eligible Beneficiaries

You may also apply for eligibility if you fall into one of the following categories:

- Certain U.S. citizens who served in the armed forces of a government allied with the United States in World War II

- Individuals with service as members in certain organizations, such as Public Health Service officers, cadets at the United States Military, Air Force, or Coast Guard Academy, midshipmen at the United States Naval Academy, officers of National Oceanic & Atmospheric Administration, merchant seaman with World War II service, and others

Restoration of Entitlement

Veterans can have previously-used entitlement “restored” to purchase another home with a VA loan if:

- The property purchased with the prior VA loan has been sold and the loan paid in full, or

- A qualified Veteran-transferee (buyer) agrees to assume the VA loan and substitute his or her entitlement for the same amount of entitlement originally used by the Veteran seller. The entitlement may also be restored one time only if the Veteran has repaid the prior VA loan in full, but has not disposed of the property purchased with the prior VA loan. Remaining entitlement and restoration of entitlement can be requested through the VA Eligibility Center by completing VA Form 26-1880.